When it comes to payroll, there’s one commonly held belief: more is always better. And while that may be partially true, recent research suggests that it’s not that simple

More than ever, workers are more concerned about pay fairness—the right amount, delivered at the right cadence.

Workers that are paid more frequently exhibit more signs of financial wellbeing than those who are paid less often; weekly-paid households borrow from credit cards 30–40% less, on average, than monthly-paid households.

There’s also an undeniable connection between wage frequency and employee retention, loyalty, and productivity. Workers that feel more financially secure due to increased pay frequency are 77% more likely to work harder and pick up extra shifts.

When workers are your product, like they are in staffing, retention is a necessary facet of success. Therefore, payroll isn’t just an administrative function, it’s infrastructure. The timing, method, and speed of your payouts affect every part of your business:

But here’s the problem: Most operators think about payroll from the inside out, often leading their strategy with, “What’s easiest for us?”

The best operators flip that: They start with the pay experience they want to deliver and then build the system to support it.

This guide is for staffing leaders who want to be among the best. We’ll define the components of a pay schedule, break down the most common pay schedules used in staffing and show you who each schedule works best for, how to stay compliant, what methods, speeds, and funding models help you deliver it, and real-world examples to help you choose the right configuration.

Whether you’re running payroll for 100 workers or scaling to 10,000, this guide will help you move from rigid and reactive to flexible and intentional.

Most staffing firms don’t set out to build rigid payroll systems. Either through limitations or because of the status quo, they inherit them.

A biweekly cadence. A direct deposit default. A “we’ve always done it this way” mentality. But what seems efficient on the surface creates hidden drag across your business:

At a glance, payroll looks simple: pick a schedule, send the money, move on.

But once you’re paying hundreds or thousands of workers across multiple roles, states, and business models, how you structure pay becomes a core part of your operations infrastructure.

The first decision isn’t “direct deposit or paycard?” — it’s this:

Is your business model built around pay frequency or pay speed?

For decades, payroll systems were built around fixed pay frequencies: weekly, biweekly, semi-monthly. Everything from funding and approvals to compliance and reporting was scheduled in advance, and workers got paid on a cadence set by the employer.

That model still works for many traditional staffing firms. But today’s labor market is shifting fast.

Platforms that serve shift-based, gig, and high-churn workforces are no longer designing around pay frequency. They’re designing around pay speed: how quickly workers can access earnings once a job is done.

If you design around pay frequency when you really need speed, two things happen:

In contrast, when you design around speed, frequency becomes flexible — something you control and layer on based on your model.

T+2 means workers are paid two business days after payroll is processed. This is the default pay speed for most legacy payroll systems and remains the most common setup for weekly or biweekly W-2 employees.

While not fast by today’s standards, T+2 is:

When you choose T+2 ACH as your pay speed, you’re committing to a system where funds land in workers’ bank accounts two business days after payroll is processed.

You run payroll on Monday → workers get paid on Wednesday.

Or run on Wednesday → pay hits Friday.

Behind the scenes, this setup depends on:

Here’s a common setup:

A light-industrial staffing company runs weekly T+2. Payroll is processed Wednesday by 2:00 pm PT; ACH direct deposits land Friday.

On most platforms, edge cases (e.g., unbanked workers, bad routing/account numbers) are handled by reprocessing via ACH once details are corrected or by cutting a physical check.

Note: If you’re using Zeal: there’s an additional, controlled fallback—admins can issue a downloadable check from the UI for exceptions, instead of waiting for ACH reprocessing or printing a physical check.

This approach works well when:

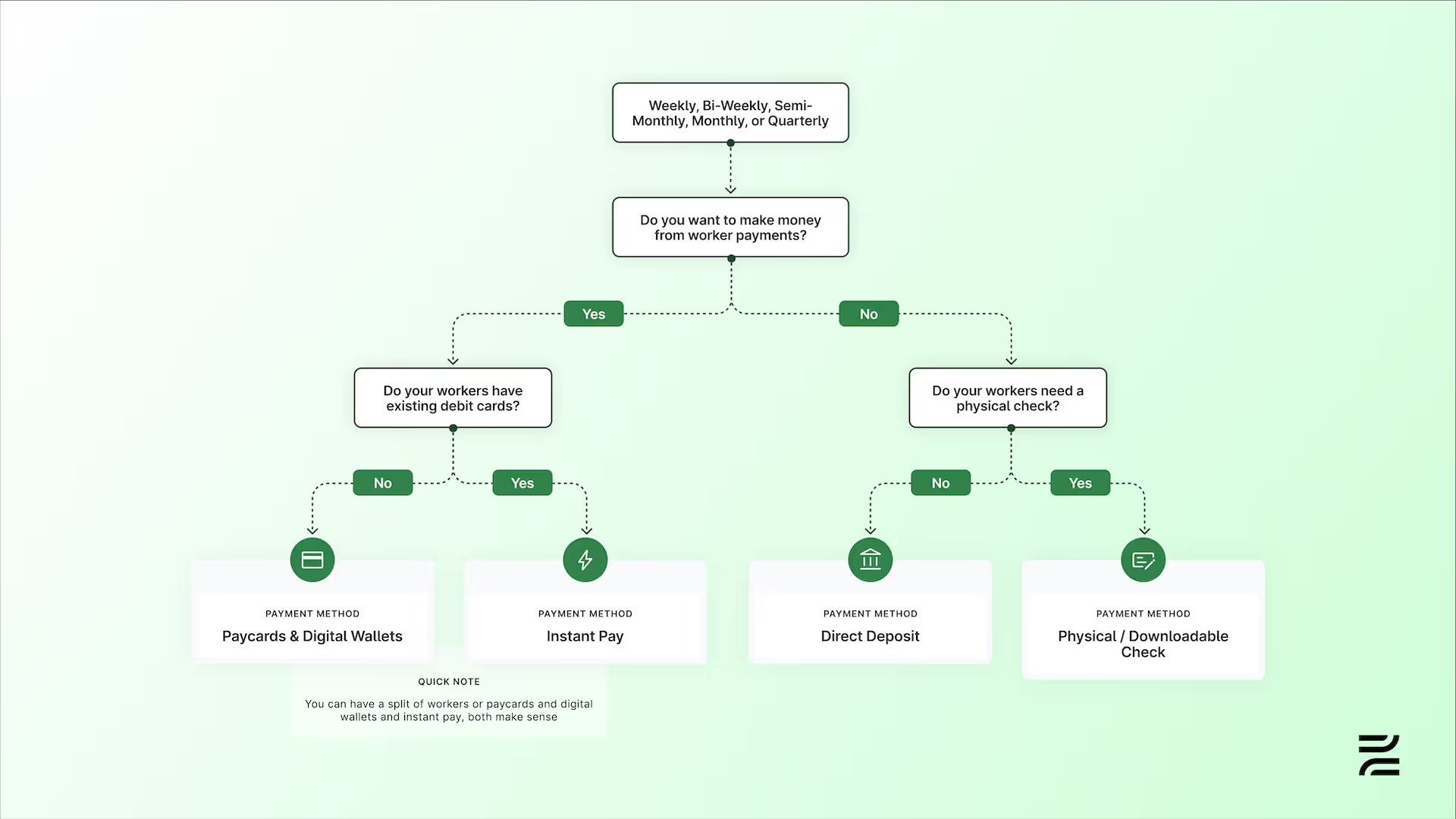

T+2 pay doesn’t limit you to just one method. In fact, Zeal supports multiple options — all timed to align with your cutoff:

T+2 works — until it doesn’t.

If you start to see:

1-Day ACH delivers wages on the next business day after you process payroll.

We seldom recommend 1-Day ACH because it’s too slow for on-demand needs—workers who need cash now won’t accept “tomorrow”—and it doesn’t offer enough upside over T+2; you take on cutoff pressure and funding complexity for only a one-day gain.

If you’re considering next-day just to look fast, skip it. Keep T+2 for the paycheck and add Instant for the moments that matter.

You finalize payroll, beat the cutoff, fund appropriately, and Zeal releases ACH credits that land next business day. In practice:

Miss the cutoff? You either shift the pay date or fall back to T+2 for that run.

Where 1-Day can break (and how to avoid it)

Stick with 1-Day if “tomorrow” solves 90% of your tickets and you want to keep a clean weekly engine. Move to Instant (next section) when your roles are shift-based, churn is sensitive to cash timing, or support volume is driven by “I need it now.”

For 1099 work, there isn’t really a “pay cycle.” There’s an event. The shift ends. The task is approved. The milestone is accepted. In a trigger-based model, that event automatically initiates the payout. Frequency becomes irrelevant; speed is the system.

Jordan wraps a four-hour event shift. The client supervisor taps “Approve.” Your platform emits a shift.approved event, calculates net payable after fees, runs fraud/velocity checks, and disburses in minutes to Jordan’s wallet or card. No batch run. No waiting for Friday. An immutable ledger entry ties the payout to the shift ID for reconciliation and reporting.

What you’ll actually need

Speed sets the experience; frequency packages it for compliance, statements, and trust.

Once you’ve chosen how fast money needs to move, decide how often you want the system to formalize pay. Frequency sets expectations, simplifies reporting, and, especially for W-2, keeps you inside the lines. In a speed-first stack, frequency is a presentation layer on top of your rails.

For W-2, frequency is constrained by state rules and worker type. Weekly or at least twice-monthly is the safest default for hourly roles across strict states; your official cycle must still produce accurate stubs, overtime by workweek, and timely final pay.

See state by state compliance guidance regarding W-2 frequency →

For 1099, frequency isn’t regulated the same way; event-driven payouts are fine. Your obligations shift to identity/tax (W-9/1099), platform policies, and clean records that tie each payment to the approved work.

If your north star is predictability (W-2 hourly across states):

Choose weekly as the official cadence. Layer Instant Pay for mid-week needs. Use 1-Day when “tomorrow” materially improves retention; fall back to T+2 when cutoffs are missed.

If your north star is operating leverage (salaried/internal W-2):

Choose biweekly for fewer runs, keep T+2. Offer Instant Pay sparingly (exceptions, emergencies).

If your north star is time-to-cash (1099/gig):

Skip the cycle. Use trigger-based instant as default, with ACH as a low-cost fallback. Provide weekly/monthly summaries for clarity—not as a gating function.

Staffing (W-2 per-diem):

Keep weekly as the official schedule. Approve time nightly. Offer Instant Pay against approved earnings; reconcile on Friday. When census spikes, switch select teams to 1-Day for “processed today, lands tomorrow” without touching the rest of payroll.

Marketplace (1099 events):

Wire payouts to the approval event. Funds hit wallet/card in minutes; finance rolls up a weekly statement for contractors and a client invoice per event batch. ACH is the opt-in “cheap but slow” lane.

When they pay you vs. how fast you pay workers.

The biggest constraint on speed isn’t always technology, sometimes it’s cash timing. If clients pay you on Prepayment or Due on Receipt, you can usually promise 1-Day or Instant without sweating liquidity. If they pay on Net 15/30/45, you’re fronting payroll before cash arrives so your stack needs a bridge (reserve or credit) and stricter cutoff discipline.

There are two clocks running:

Every decision in this guide lives in the space between those clocks. The farther apart they are, the more your stack needs prefunding, a reserve, or an approved credit line.

Miss a cutoff and you either move the pay date or fall back to a slower lane; the UI should gray out ineligible speeds and explain why.

If your clients are Net 30 and your workers expect Instant, you need reserve or credit. If you keep missing 12:50 pm PT on 1-Day, either move your internal approvals earlier or set the official promise to T+2 and layer Instant for urgent cases. If Finance can’t tie every payout to a job/shift ID in two clicks, tighten the ledger before you scale speed.

Weekly payroll still reigns in staffing. Why? Some would say tradition, most would say compliance. In many states, especially for W-2 hourly and manual labor roles, weekly pay is the law. In others, it’s what workers expect. And in high-turnover industries like healthcare, light industrial, and hospitality, it’s often the difference between retaining workers and constantly refilling the funnel.

If you staff hourly, per diem, or shift-based W-2 roles, weekly pay should be your default.

Many states mandate weekly pay for certain worker categories — especially manual labor, hospitality, and hourly roles. Even when not explicitly required, some states place restrictions on how infrequently you can pay.

Here’s what staffing operators need to watch for:

⚠️ Note: In most of these states, “manual labor” includes a wide range of staffing placements — from janitorial and warehouse to healthcare aides and delivery drivers.

Your payroll stack is your business infrastructure. It’s not just about compliance—it’s a strategic lever for retention, trust, and operational efficiency. And in staffing, where workers are the product, the stakes are even higher.

Here’s what matters most:

Bottom line: The best staffing operators treat payroll not as a cost center, but as a product. One that’s fast, flexible, and built around the needs of modern workers—not just the constraints of legacy systems.

Want a payroll system built for speed, compliance, and scale?

Zeal powers modern staffing operations with flexible pay configurations, real-time payout options, and built-in compliance guardrails—so you can run payroll your way, without the chaos.

👉 Book a demo to see how it works.

A pay schedule defines when workers are paid (daily, weekly, bi-weekly, etc.), how fast funds are delivered, and what operational cutoffs apply. In staffing and labor platforms, pay schedules must align with time capture, approval workflows, payroll funding, and client billing, not just calendar dates.

Modern workforce platforms treat these as separate configuration layers, allowing faster pay without changing statutory pay frequency.

By decoupling pay speed from pay frequency.

Platforms like Zeal allow companies to:

This preserves compliance while improving worker experience.

Pay schedules break when:

Scalable platforms treat pay schedules as infrastructure, not a payroll setting.

Yes—if implemented incorrectly. Risks include:

Employer-provided models integrated directly into payroll reduce these risks.

Yes. Some states mandate:

Staffing companies operating across states need state-aware pay logic, not static schedules.

Yes. Faster pay can be:

The key is native integration, not bolt-on payment tools. Find out how to monetize worker payments.

Pay schedules determine:

Faster worker pay without aligned billing logic creates cash-flow strain. Integrated payroll-to-billing workflows prevent this mismatch.

No.

A worker can be on a weekly pay schedule and still receive instant pay for completed shifts.

Because they were built for:

High-velocity staffing requires dynamic pay rules, API-driven configuration, and real-time funding logic—capabilities legacy systems weren’t designed for.

Key capabilities include:

Share this:

Zeal is a financial technology company, not an FDIC insured depository institution. Banking services provided by Bangor Savings Bank, Member FDIC. FDIC insurance coverage protects against the failure of an FDIC insured depository institution. Pass-through FDIC insurance coverage is subject to certain conditions.

Mastercard® Debit Card is issued by Bangor Savings Bank, Member FDIC, pursuant to license by Mastercard International Incorporated. Mastercard is a registered trademark, and the circle design is a trademark of Mastercard International Incorporated. Spend anywhere Mastercard is accepted.